If you’ve been paying attention you’ve probably heard something about the countless jobs artificial intelligence will eventually take over from us mere mortals. So when I dove into this little exercise I was really hoping to find that the role of “financial planner” would not be one of those casualties. While I don’t think I’m on the chopping block quite yet, what I found was pretty impressive and a little alarming.

I started off by prompting the program with a retirement scenario in which I pretended to be 63 years old with a $1.5 million nestegg saved between me and my spouse. I gave the program some basic details around our imaginary situation, and requested that it create a 25 year retirement plan for us. You can read the full prompt below if you’re interested.

My intention with this first prompt was to start off vague and open ended because that’s typical when starting a retirement planning conversation with someone new. A big part of a financial planner’s job is asking the right questions to learn about individual preferences and intangibles, while also collecting the necessary data to start building a plan. So, I was definitely interested to see the breadth and depth of the questions the program would come up with and compare it to my own discovery process.

ChatGPT absolutely nailed this data collection portion to the point that I’m fairly convinced the program directly referenced the Certified Financial Planner online curriculum. The follow up questions were basically verbatim what each CFP is taught to request before starting a plan. Within seconds of entering my initial prompt nine follow up questions were neatly presented on screen with underlying bullet points explaining the key points of consideration for each question. Good job Mr. Roboto!

I took a few minutes to answer each of the follow up questions, and while doing so I decided to get a little tricky. In filling out my responses I threw in some intentional red flags just to see if the program would pick up on them. For instance, I stated that my current portfolio was 75% stock which is typically considered a “no-no” for someone about to retire. I wanted to see if and how the program would approach that element of my plan. Additionally, I mentioned that I wanted to leave $1.2 million of legacy assets to our children, which I knew would be quite unlikely given the level of retirement spending I had previously requested. Game on all-knowing supercomputer!

It came back with 6 more follow up questions that dug a little further into my initial set of responses. The questions were more niche and requested specific info regarding social security amounts, tax filing status, and medical plan preferences. All-in-all I remained impressed with the level of specificity the program was looking for, but at this point I was more anxiously awaiting the first output of my plan. Mind you, I was about 5 minutes into this ordeal.

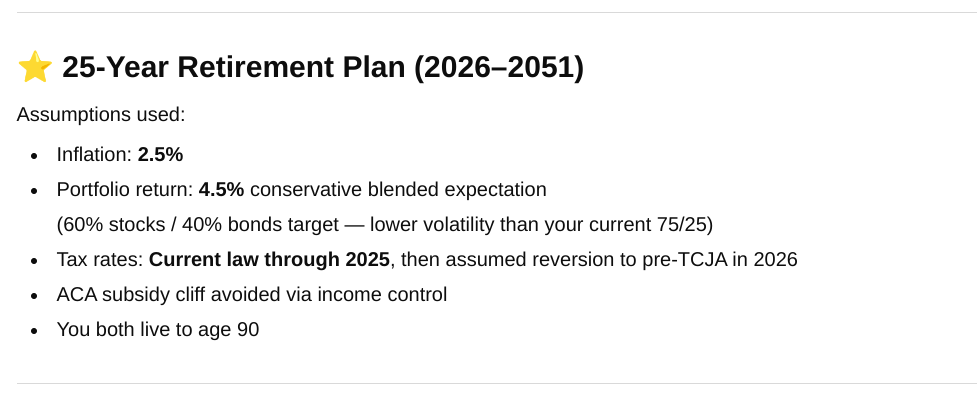

Finally (after another 10 seconds) it was here. My very own AI generated retirement plan! The first item of note was its length. When I copied and pasted the output into a word document it came to twelve pages, but more important was assessing the actual substance of the plan. The output started by listing the top priorities of my plan, all of which were simply a reflection of my prior responses. Nonetheless, it’s common practice and extremely useful to list planning priorities at the start of a plan in order to ensure that all parties are on the same page, and the advisor understands the clients goals. The next section listed the underlying assumptions baked into the plan such as the assumed inflation rate, average annual portfolio return, and tax rates. Also, common practice in real-life plan presentations. So far, so good.

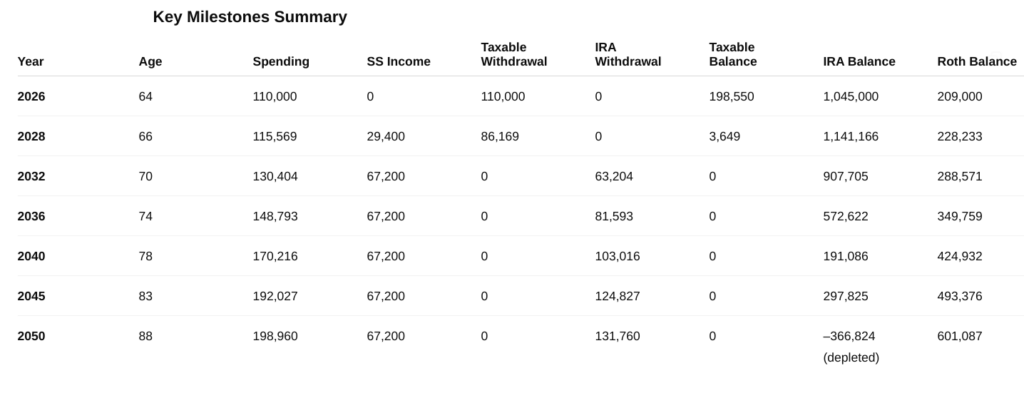

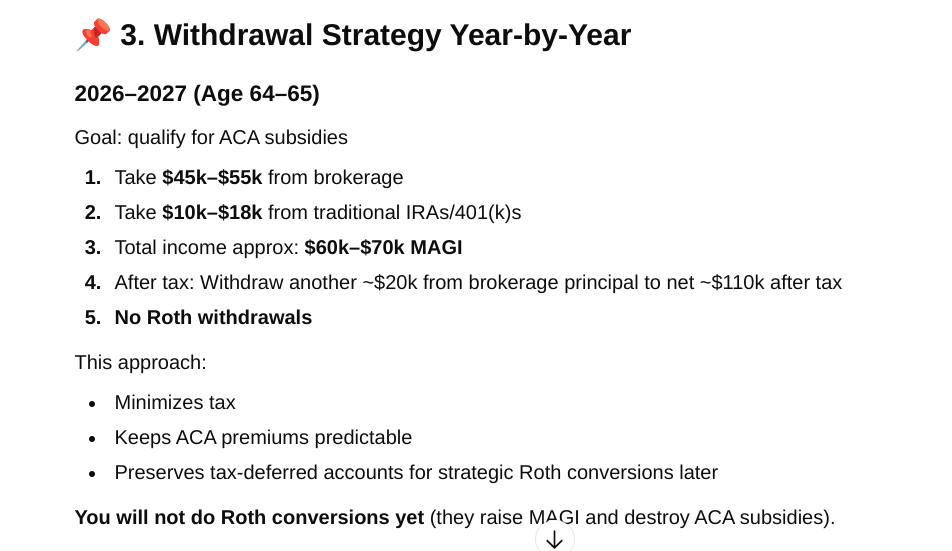

From here the program began actually laying out its specific recommendations conveniently arranged in seven numbered headings with bullet points providing specifics for each one. In my opinion this is where things could go a bit south. These foundational recommendations in areas like Social Security timing, withdrawal strategy, and investment strategy tend to be the biggest factors in determining the outcome of a plan. Almost all of these decisions will have a long-term impact on one’s finances, and several cannot be undone once they are made. Each of these topics typically warrant their own individual planning discussions in order to hone in on the right solution. Therefore, I found it a little cavalier for a chatbot to be making these weighty recommendations for someone who might not understand the full gravity of these decisions. That said, the program was only doing what it was told, so it came time to assess the actual viability of its plan.

There’s no sense in burying the lead here. The plan it produced was extremely feasible. In order to test ChatGPT’s proposed plan I plugged the same facts and its recommendations into my planning software, and its plan produced a 93% probability of success. It accurately identified the portfolio allocation redflag, and recommended a more conservative allocation that still accomplished my desired retirement income level. Additionally, it provided several forms or charts and tables illustrating projected account balances and cashflows year-by-year.

However, the plan fell short in a few areas too. The program failed to address the fact that I would likely come up well short of my legacy gifting goal. It simply didn’t address that area of my plan, which tends to be a core element of many of retirement plans today. It also assumed the wrong Federal tax rates. This is an interesting little glitch due to the fact that the free version only utilizes information that has been publicly available for six months or more. Therefore, it didn’t account for the recently passed tax bill in July of 2025. This I view as a real problem being that it could have led to a catastrophic tax season for my first year of retirement. With that said, the workability of its plan and the level of information it provided within minutes was still nothing short of impressive.

Now, selfishly circling back to my original concern, I’m not terribly fearful I’ll be hitting the unemployment line anytime soon. While there’s no denying that ChatGPT came up with a sufficiently viable plan for me in record time, the fact remains that implementing and adapting the plan year after year is far more difficult than creating it. Not to mention the program made some pretty lofty assumptions about my ability to understand its terminology and carry out its recommendations.

For instance, its first recommendation for my 2026 income was to “Take $45k-$55k from brokerage.” What does that mean? What’s a brokerage? What do I sell? How do I rebalance? What if the market is down? The plan was littered with bullet points like this one that assumed a pretty high level of technical know-how with a dash of blind faith. In essence, the plan is only as valuable as one’s confidence and ability to actually implement it successfully.

I’m not saying there won’t come a time where artificial intelligence plays a much larger role in helping people reach their financial goals. In fact, after this exercise, I’m quite optimistic about its usefulness for that purpose. At the very least, this run-through proved to me that ChatGPT can be an incredibly powerful tool to sense-check your financial trajectory, or analyze certain planning strategies for those in the accumulation stage. However, in the high stakes realm of retirement planning where every detail matters, I think many will continue to prefer and rely on the council of fellow humans for life’s biggest financial questions. Call me old fashioned, but for now I think I’m safe.