If you’ve ever had a retirement plan prepared, you probably came across an interesting yet ambiguous metric known as “probability of success”. It’s often displayed front and center as a percentage ranging from 0 to 100, almost like a test score. And much like a test score, it’s easy to assume that anything less than perfect means something has gone wrong. I can appreciate the former student in all of us striving for straight A’s. However, in the realm of retirement planning, I’d argue you’re better off aiming for B’s and C’s if you really want to pass your retirement with flying colors.

What is Probability of Success?

In order to understand the significance of the probability of success metric, we have to get in touch with our inner nerd. It starts with understanding how probability of success is calculated and what it actually represents. At its core probability of success is an estimate of how often your plan “works” when tested against different market conditions.

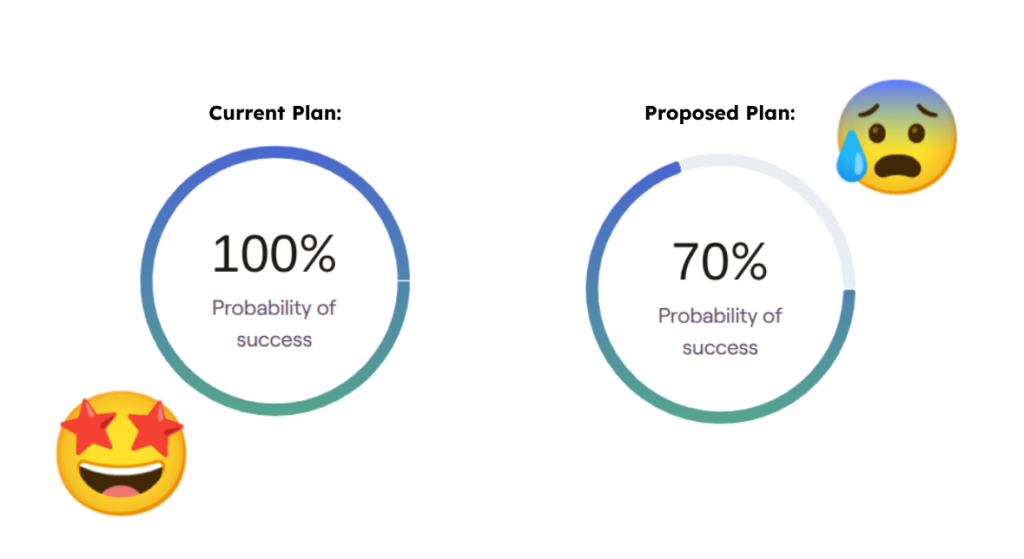

For example, let’s say you have a one million dollar nestegg, and your retirement plan assumes you will only withdraw $30,000 per year from those assets. That is a very small portion of the portfolio, making it highly sustainable even in very poor markets. Therefore your probability of success will be very close to (if not) 100%, because there is virtually no chance you would ever need to deviate from that planned withdrawal amount. Basically, your plan is expected to be “successful” no matter what happens in the market.

Alternatively, if you plan to take $50,000 per year from that same one million dollar nestegg, that puts a bit more stress on the portfolio to perform positively throughout your retirement. It’s a bit less certain that you can sustain that annual withdrawal no matter what. Therefore, at this higher withdrawal amount the plan’s probability of success likely drops into the range of 70% (almost failing according to your teacher’s standards).

Now back to math class where the original question of how exactly “probability of success” is calculated. One of the big advantages financial planning software offers is the ability to run hundreds of market scenarios instantaneously. It starts with the advisor constructing a client’s plan, and building in all the assumed annual withdrawals. Then the software runs that single plan through 1,000 different mutli-decade market scenarios; some very good market scenarios, some very bad, and lots in between. This serves as a way to stress test the plan across a wide range of possible futures.

The end product of this stress test is a single percentage representing how often the plan “worked” or “held up”, in which case there was no need to deviate from the planned withdrawal amounts. So, a 75% probability of success means that three out of every four scenarios required no deviation from the planned withdrawals. That leaves a quarter of the scenarios where a downward adjustment to withdrawals was required at some point throughout retirement due to very poor market conditions.

What is Success As a Retiree?

Here’s where we get into the key questions of Retirement Philosophy 101. Is it worth sacrificing what could be tens of thousands of dollars per year in retirement income in order to achieve a 100% probability of success for your plan? How much retirement income and lifestyle flexibility is being left on the table for the sake of absolute certainty? Or, flipping these questions around, how much uncertainty are you willing to stomach in order to enjoy more retirement income in the present. These answers will be different for everyone, hence its philosophical element.

A growing number of advisors are recognizing that formulating a plan with a 100% probability of success is often not in the client’s best interest because it leads to substantial underspending throughout retirement. In fact, there are advisors who are comfortable recommending a plan with 50% probability of success depending on the client’s tolerance for downward adjustments to income. In my own experience, I find it more common than not for clients to be willing to stomach some reasonable level of uncertainty if it means higher income and more lifestyle flexibility now. Especially once they understand that an 80% probability of success does not mean a 20% chance of “running out of money”. Instead it translates to a one in five chance that at some point throughout their retirement they may have to accept a temporary decrease in their income due to poor markets.

For the final exam, take a moment and think about what “probability of success” means to you now having the knowledge of its nuances. Do you lean towards more income with more uncertainty, or less income with less uncertainty? What kind of student will you strive to be throughout your retirement?